The BNPL application market has significantly grown over the past six years. Its share increased almost 7 times – from 0.4% to 3%. It is extremely convenient for people to pay for purchases in installments. During the pandemic and economic instability, such a service is more relevant than ever, so customers are actively using BNPL applications. In the US, Klarna is the undisputed leader in terms of downloads, but there are high-quality alternatives on the market. Let’s consider three BNPL apps with different payment terms.

This BNPL solution is a mobile application for purchasing goods from partner stores on a “buy now, pay later” basis. A user registers in the system, explores the catalog of an online store, selects the necessary product, and places an order. The client sets the most suitable installment option (repayment in one or four stages) and sends a request. The system and the administrator approve the purchase and the customer completes the order. They receive an email with a payment plan. The user also monitors at what stage of delivery the product is and at what time it will arrive.

The application notifies the user about the upcoming payment by the scheduled dates. If the client delays the payment, they will be assigned a commission. An archive of purchases and payments is available in the reminders and notifications module. If the buyer has questions, they turn to the chatbot in the “Support” section. The application also analyzes user preferences and generates unique offers for each client. Thanks to the implementation of such functions, trading platforms increased conversion by 14%, and 25% of users repeat purchases. More than 13 million people actively use the BNPL application.

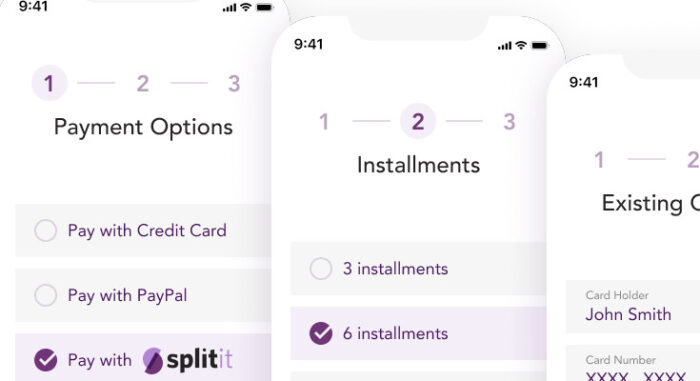

Interest-free payments with Splitit credit card

Splitit is a BNPL solution that helps customers easily buy goods in installments. To do this, users need to have a credit card and the required amount on it. In this case, you do not need to obtain approval for the purchase of goods.

A user visits pages of partner stores (Purple Mattress, Nectar, Woo Commerce, Shopify, etc.). When ordering goods, they indicate Splitit, select a convenient installment option, and enter credit card details. The platform generates payments that will be automatically debited from the card monthly, within a specified period. If the client does not make a payment on time, Splitit does not remove commissions or penalties. But this can be done by the bank that issued the credit card.

When a person buys a product with Splitit, a sum covering its entire cost is “blocked” on the credit card. This means that the money cannot be spent on other things, and it looks like an incomplete credit card transaction. On the day of payment, the money is debited from the credit card and the “pending” amount is paid off. The process will end when all payments are made. There is no need to worry that scammers will steal money: the Splitit platform has a PCI security standard – DSS level 1.

Thus, buyers do not need to take out additional loans to buy costly goods, moreover, they can do everything interest-free. Splitit offers them to purchase the desired item by holding credit card funds until the amount is paid off.

Perpay interest-free installment plan pegged to salary

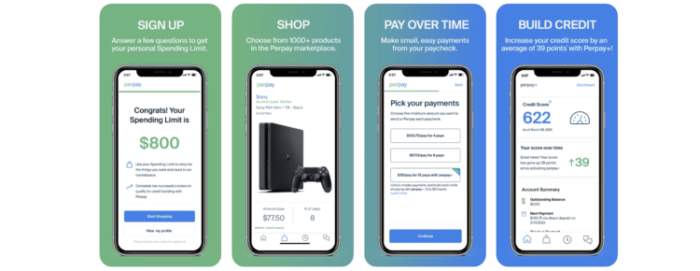

The Perpay service has two important missions: to help buyers purchase large goods in installments and to improve their credit rating. As a rule, the application is used by people who want to “rehabilitate” themselves in the eyes of the creditor bank. Perpay does not check credit history, but the user needs to have worked at the same company, enterprise, or institution for at least 3 months, set up direct deposit, and earn at least $15,000 a year.

To allow a user to make large purchases, the service “verifies” this person by offering them a minimum credit limit of $200. If the buyer manages to pay off the funds on time after purchasing the item, the limit is increased to a maximum of $2,000. The client can “divide” purchases into 4, 8, 16, or 18 payments.

Timely payment strengthens the credit rating by 39 points because information about the client’s reliability is transmitted to Experian and Equifax, the largest credit bureaus. In this way, people correct their credit history to receive financial assistance for serious purchases in the future.

Perpay does not use credit or debit cards but works directly with the payroll. This means that the paid goods are not sent to the buyer until they make the first payment the day after receiving their salary. Thus, the service checks whether it is possible to trust the client and offer them large amounts of money. More than 1,000 online stores and four million users cooperate with Perpay.

Conclusion

BNPL apps support a new convenient format for buying goods when a user is unable to pay the full price. Such platforms offer different conditions: limits on the amount, solvency check, number of payments, repayment methods, or commissions. Therefore, any user will be able to find a suitable solution and buy goods as needed. Thus, they don’t have to wait until they earn the required amount of money. They can start using the product without affecting their budget.

The popularity of BNPL platforms is growing rapidly because users do not want to burden themselves with additional bank loans. According to Statista experts, by 2024, the size of the BNPL market in America will grow by 1200%. Users like these trending solutions for their simplicity and quick payment capacity. This is exactly what the modern consumer needs.